|

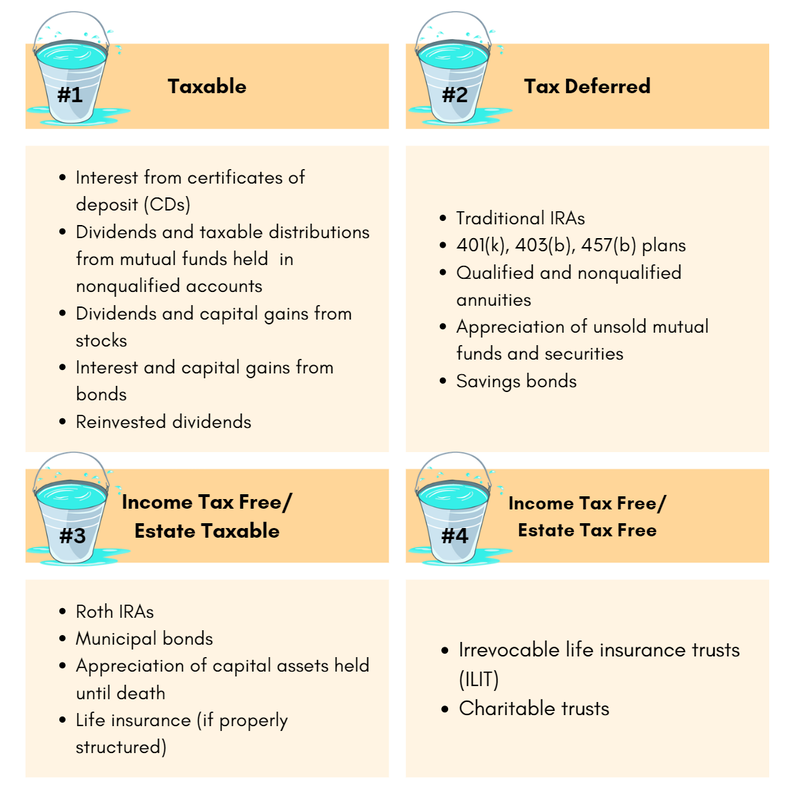

Over the past few weeks you can take what we’ve learned and compare it against your career path. Part one of our series focuses on individuals just starting their first jobs and are overwhelmed with the constant inflow of information. Part two is when you’ve had a couple of years to digest the information and want to invest more productively. The last and third part of our series is aimed toward those individuals who are ready to start withdrawing from these accounts. As we explained in part two, tax liabilities for each account varies and withdrawing from them can negatively impact your tax situation. For example, some investors will withdraw funds from their brokerage account to make larger purchases (i.e., home, car, etc.) but if the investments are held less than 12 months there are tax implications. Even more, if you are looking to pull money from a retirement account the amount is restricted and is only for first-time homebuyers - this is unless you are willing to take an additional penalty on top of the ordinary income. The Bucket System One traditional method for withdrawing money is called the bucket system. This strategy is based on the philosophy that over time you’ll receive more income as you age and this is partly due to earnings from social security and required minimum distributions. This system breaks up account types into taxable, tax deferred, and tax free. Each of these tax liabilities were discussed in Part two of our series. Most investors will begin withdrawing from Bucket 1: Taxable accounts to subsidize their income as they age. After depleting the funds from Bucket 1, you’ll ideally move to Bucket 2: Tax Deferred withdrawals. In some cases - like required minimum distributions (RMD) - you would need to take a distribution prior to the depletion of your taxable funds (e.g., bucket 1). After that point, you can offset your RMD and reduce the amount taken from Bucket 1. If you have disbursed everything from your first and second bucket, you’ll move on to the Bucket 3:Tax Free which will have the most favorable tax treatment. In the example below, you will see there is a fourth bucket which is specific to reducing your estate’s taxable liability after you’ve passed. We haven’t discussed much about this but in our life insurance series later this year we’ll dive into this strategy.  This system is not fool proof and depending on your financial situation a second opinion can save you money that others would have left on the table. I work with individuals to help create plans around their financial goals and offer guidance on how to take advantage of the opportunities within their portfolio. For a personalized plan, schedule an appointment with me today and to learn more about Strategies for Retirement use the download button below for a FREE pamphlet. If you fail to plan, you plan to fail.

0 Comments

Leave a Reply. |

Archives

July 2024

Categories |

RSS Feed

RSS Feed

Financial Services are offered through Family Retirement LLC, a registered investment advisor. Family Retirement LLC is a registered investment advisor in the State of Washington. Family Retirement LLC may not transact business in states where we are not appropriately registered, excluded, or exempted from registration. Individual responses to persons that involve either the effecting of transactions in securities, or the rendering of personalized investment advice for compensation, will not be made without registration or exemption. Neither the firm nor its agents or representatives may give tax or legal advice. Individuals should consult with a qualified professional for guidance before making any purchasing decisions.

Privacy Policy | ADV Part2A

425-610-9226

1700 Westlake Avenue North Suite 200

Seattle, WA 98109

Copyright © 2024

Privacy Policy | ADV Part2A

425-610-9226

1700 Westlake Avenue North Suite 200

Seattle, WA 98109

Copyright © 2024

|

|

|