|

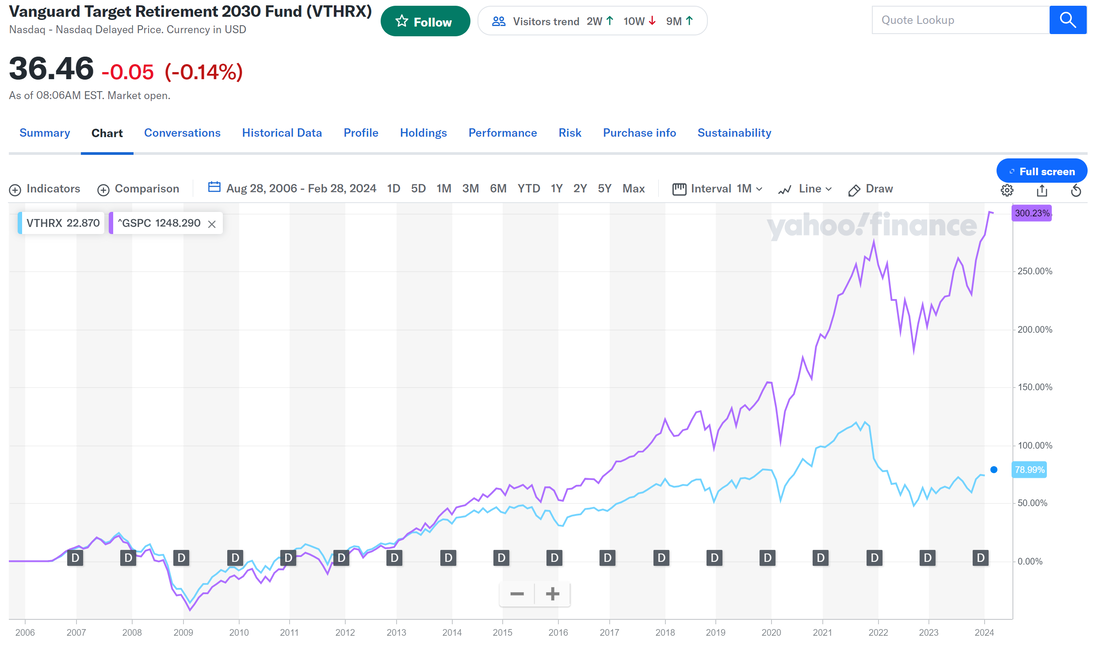

Stop setting Millennials and Gen Z up for investment failure; here's how to get more out of your 401k. Company-sponsored investment plans, commonly known as 401k, serve as the initial investment tool for most Millennials and Gen Z. If you haven't purchased a house yet, they could represent the primary source of your net worth. These sleeping giants are supposed to form the foundation for retirement, but many younger investors are being shortchanged. The issue lies in automatic investments in target-date retirement funds. What are target-date retirement funds? Target-date retirement funds consist of a pre-selected mix of stocks and bonds based on your planned retirement date. They typically include four groups: US Equities, International, US Bonds, and International Bonds. For instance, if you have 40 years until retirement, your target-date fund might allocate 90% to stocks and 10% to bonds. As you approach your retirement date, the allocation shifts, aiming for a balance of 60% stocks and 40% bonds. The idea is that, closer to retirement, a more conservative approach is adopted, with bonds serving as a less volatile investment option. However, for the past several years, bonds and developed international equities have consistently underperformed, resulting in diminished upside potential. Based on the information below, if you had started your job in 2006 and invested in a target-date retirement fund, you would have incurred a loss of 215%.  Source: Yahoo Finance chart of VTHRX compared to GSPC (S&P 500) between Aug. 28, 2006 and Feb. 28, 2024. In no way is this a diverse portfolio; we will look further into this in Part 2, 'When Does a Diverse Portfolio Matter?' If you are using this as your benchmark, you are not meeting your goal and may be pushing back your retirement date even further.

What should you do? Align your investment goals with a benchmark. Within your 401k, there are options for Large Cap Equity, Mid Cap Equity, Small Cap Equity, and International investments. Research these options, considering their costs, potential upside, and how well they align with your retirement goals and timeframe. Mark your calendar to regularly re-evaluate performance. While it's easy in theory, putting it into practice can be challenging; the better you are at creating and sticking to a schedule, the more you'll see your portfolio grow. Hot tips: While you might be locked into changing your previous allocations for 60-90 days, future contributions can always be adjusted. Set your calendar for 2-3 days before your pay period, so changes will take effect for upcoming paychecks. If you notice a market decline, leave it in a stable value fund and allocate it to the next payroll. None of this will come naturally, but over time you'll become familiar with the platform you're using. And, as always, feel free to come to me with questions. Helping those just entering the workforce invest like a pro is one of my favorite things.

0 Comments

Leave a Reply. |

Archives

July 2024

Categories |

RSS Feed

RSS Feed

Financial Services are offered through Family Retirement LLC, a registered investment advisor. Family Retirement LLC is a registered investment advisor in the State of Washington. Family Retirement LLC may not transact business in states where we are not appropriately registered, excluded, or exempted from registration. Individual responses to persons that involve either the effecting of transactions in securities, or the rendering of personalized investment advice for compensation, will not be made without registration or exemption. Neither the firm nor its agents or representatives may give tax or legal advice. Individuals should consult with a qualified professional for guidance before making any purchasing decisions.

Privacy Policy | ADV Part2A

425-610-9226

1700 Westlake Avenue North Suite 200

Seattle, WA 98109

Copyright © 2024

Privacy Policy | ADV Part2A

425-610-9226

1700 Westlake Avenue North Suite 200

Seattle, WA 98109

Copyright © 2024

|

|

|